Wednesday, April 14, 2010

Quote

Insurance is always a Mistake. If you buy and nothing happens, it is a Small mistake. Don't buy and something happens, that is a BIG mistake.

Tuesday, April 13, 2010

New Policy 2010 - outlook

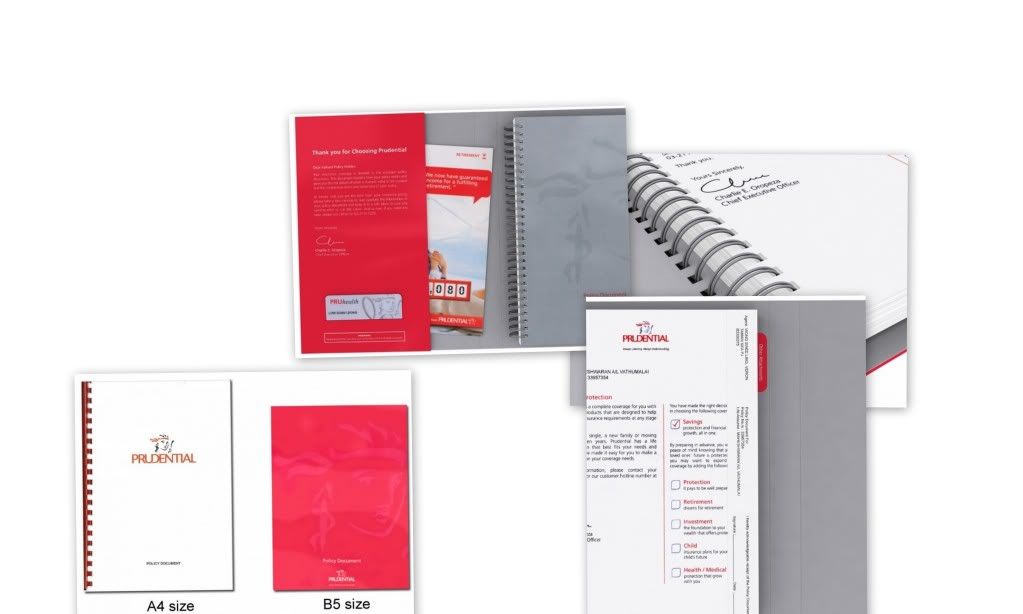

The new outlook of policy document comprises a jacket to house the policy document, slot to insert medical cards and also a pocket to insert loose items such as MHI Booklet and also endorsement slips in the future. The whole package of the policy document will come sealed in a plastic cover. All policy documents and endorsement slip will be in B5 size which slightly smaller compared to current A4 size which would again make it easier to carry the policy documents around.

The launch date of this new policy document outlook is on the 5th of April 2010

Monday, April 12, 2010

Should I Buy Medical Insurance

Should I buy medical insurance when I’m already covered by my employer? This is a common question I get and I understand why you might ask it.

There are 2 things on your mind. First, should I pay my own money for something I might not need until I retire and secondly, should I depend on the company cover? These are 2 main consideration.

Working as an employee have its good points and one of the perks is that you get group medical insurance. Employers provides such cover to retain staff, to attract talent and to avoid paying medical bills out of their own pocket.

Even so, I firmly recommend my customers to have some form of individual medical insurance because:-

- employers can and will change the medical insurance benefits they give to you. Normally it is done without your knowledge until you need to make a claim

- insurance companies change their terms (the fine print) without you or even your employers knowledge

- your past medical history automatically excludes you. In big organizations, you don’t even fill up any form. Unless your company is buying a big policy on you (usually for top management staff only). At the point of making a claim, some insurance will point to a pre-existing illness and you can’t make any claim

- your employer or your spouse’s stops offering insurance for you or your family

- you might suffer a critical illness like cancer or stroke, and the amount provided by your employer is not sufficient

Having you own medical insurance means you are in control and have a backup cover. Besides that, here are some situations which you might end up needing to seek affordable individual medical insurance:

- you lose (or quit) your job

- you have insurance through your spouse, and they lose or quit their job

- you change jobs, and your new employer has a waiting period before you become eligible for coverage

- you decided to retire early

These are some reason you should think about when you ask yourself “Should I buy medical insurance”

36 Critical illnesses – Crisis Cover

What is Crisis Cover?

Event when you are diagnosed as suffering from one of a range of 36 critical illnesses and and survive for 30 days. Prudential will compensate you with certain amount based on your premiums. For example, minimum RM20,000

What are the 36 illnesses are covered by the Crisis Cover plans?

Crisis Shield / Crisis Cover is the plan you must have in your Life Insurance, please make sure you know how much your benefits if you are diagnosed with 36 critical illnesses.

Event when you are diagnosed as suffering from one of a range of 36 critical illnesses and and survive for 30 days. Prudential will compensate you with certain amount based on your premiums. For example, minimum RM20,000

What are the 36 illnesses are covered by the Crisis Cover plans?

- AIDS as a result of a blood transfusion

- Alzheimer's Disease

- Aorta Surgery

- APALLIC Syndrome

- Aplastic Anaemia

- Bacterial Meningitis

- Benign Brain Tumour

- Blindness

- Brain Surgery

- Cancer

- Chronic Liver Disease

- Chronic Lung Disease

- Coma

- Coronary Artery Disease Requiring Surgery

- Deafness

- Encephalitis

- Full Blown AIDS

- Fulminant Viral Hepatitis

- Heart Attack

- Heart Valve Replacement or Repair

- Kidney Failure

- Loss of Limbs

- Loss of Speech

- Major Organ Transplant

- Major Burns

- Major Head Trauma

- Motor Neurone Disease

- Multiple Sclerosis

- Muscular Dystrophy

- Other Serious Coronary Artery Disease

- Paralysis

- Parkinson's Disease

- Poliomyelitis

- Primary Pulmonary Arterial Hypertension

- Stroke

- Terminal Illness

Crisis Shield / Crisis Cover is the plan you must have in your Life Insurance, please make sure you know how much your benefits if you are diagnosed with 36 critical illnesses.

What is Life Insurance - Newbie’s

We start we definition of Life Insurance

Life Insurance

Life insurance is an insurance coverage that pays out a certain amount of money to the insured or their specified beneficiaries upon a certain event such as death of the individual who is insured

Basic coverage for all type Life Insurance

1. Sum Assured

2. Coverage for Critical Illness

How many types of Life Insurance available?

Basic type's policies are

Life Insurance

Life insurance is an insurance coverage that pays out a certain amount of money to the insured or their specified beneficiaries upon a certain event such as death of the individual who is insured

Basic coverage for all type Life Insurance

1. Sum Assured

2. Coverage for Critical Illness

How many types of Life Insurance available?

Basic type's policies are

- Term insurance - This offers insurance protection for a limited period only whereby the money is paid up if you pass away or if you suffer total and permanent disability.

- Whole life insurance - Life-long protection and premiums are paid throughout your life and the money including any bonuses will be paid when you pass away or suffer total and permanent disability.

- Endowment - A combination of protection and savings whereby the money will be paid at the end of a specific period upon your demise or if you suffer total and permanent disability.

- Investment-linked - For investment-linked insurance, your premium is used to buy life insurance protection and units in a fund managed by the life insurance company. The benefits paid to you or your nominee will depend on the price of the units at the time you surrender your policy or when you pass away.

- Life annuity plan - Series of payments paid to you until you pass away. Types of annuity include immediate annuity or deferred annuity.

- Supplementary rider/cover - A rider is a supplement attached to the basic insurance plan such as endowment or whole life.

- Mortgage reducing term assurance (MRTA) - An insurance protection plan that covers the repayment of an outstanding property loan to the financial institution in the event of untimely death, disability or critical illness of the borrower.

PRUcash Double Reward

By Azrul

Triple of 2% is a Reality

The current fixed deposit rates of 2010 are a low return. What worse is the bank rate is dropping

It is Time to Change

It is possible to earn 3% or even up to 6% per annum GUARANTEED !

PruCash Double Reward from Prudential is a product designed to help you maximize your Fixed Deposit savings.

Now you don't need to take unnecessary investment risk e.g. stocks, unit trusts.

Now you don't need to take unnecessary investment risk e.g. stocks, unit trusts. Risking volatile market rates and speculations.

Please Follow my Illustration

Assuming that today Mr Kamal Age 30 have RM10,000 that he want to into fixed deposit.

Mr Kamal need to put the money without movement in the bank before earning 2.5% interest.

That is 4 times return in the FIRST YEAR itself !

Excited ? Want to know more ?

36 Jenis Penyakit Kritikal

Berikut adalah senarai 36 penyakit kritikal

- Serangan Penyakit Jantung

- Penyakit Koronari Arteri Yang Memerlukan Pembedahan

- Strok

- Kanser

- Kegagalan Ginjal (Buah Pinggang)

- Penyakit Lumpuh/Paraplegia

- Pemindahan Organ Utama

- Sklerosis Pelbagai / Berbilang

- Hepatitis Virus Fulminan

- Hipertensi Arteri Pulmonari Utama

- Koma

- Buta

- Penggantian Injap Jantung

- Pembedahan Aorta

- Penyakit Alzheimer

- Hilang Pendengaran / Pekak

- Hilang Kebolehan Bertutur (Bisu)

- Kebakaran Parah

- Penyakit Membawa Maut

- Aids Akibat Transfusi Darah

- Penyakit Motor Neuron

- Penyakit Parkinson

- Penyakit Hati Yang Kronik

- Penyakit Peparu Yang Kronik

- Anemia Aplastik

- Distrofi Otot

- Poliomielitis

- Meningitis Bakteria

- Tumor Otak Benigna

- Ensefalitis

- Full Blown Aids

- Lain-Lain Penyakit Koronari Arteri Yang Serius

- Pembedahan Otak

- Sindrom Apalik

- Trauma Kepala Utama

- Kehilangan Tangan Atau Kaki

Subscribe to:

Posts (Atom)